Although it's not as newsworthy as Guy Fawkes attempting to blow up the Houses of Parliament, the Bank of England still stole the headlines on the 3rd November when it raised interest rates from 2.25% to 3%; the biggest hike since 1989.

But what does this mean for the world of investing? Are high interest rates a good or bad thing? And how should you invest accordingly?

Stick around and we'll fill you in on as much interesting (sorry) info as possible.

Oh, and for you busier folk who need the answers now, don't say we didn't think of you:

Are high interest rates a good or bad thing?

Before getting into whether you should invest and how to go about doing it, it's important to know if high interest rates are a good or bad thing for you.

Whether it is good or bad, depends on your financial situation. Let’s take a look at some examples.

✅ Generally, high interest rates suit people who:

Have a lot of cash

Don't have a mortgage

Are free from other forms of debt such as credit loans

Why is this?

Well, when interest rates increase, the banks offer better rates for savings accounts, and so people's cash earn a higher interest when in an account like a cash ISA.

Of course, banks will up the interest payments on loans they distribute, such as mortgages. If someone has paid off their house, or even rents, this is something they won’t have to worry about. The same logic applies to other forms of debt.

❌ High interest rates are bad news for people who:

Are applying for a mortgage

Are paying off a mortgage (especially when on a variable mortgage)

Have other forms of debt, such as credit loans

Receive a low income/ have a lack of cash

Often, higher interest rates suit older people as they've had a chance to build their wealth and pay off debts throughout their career.

How do high interest rates affect me?

When interest rates increase, it helps bring inflation back down to our target, which is 2%. The hope is, we'll all experience a reduction in cost in everyday items such as food, clothing and utility bills.

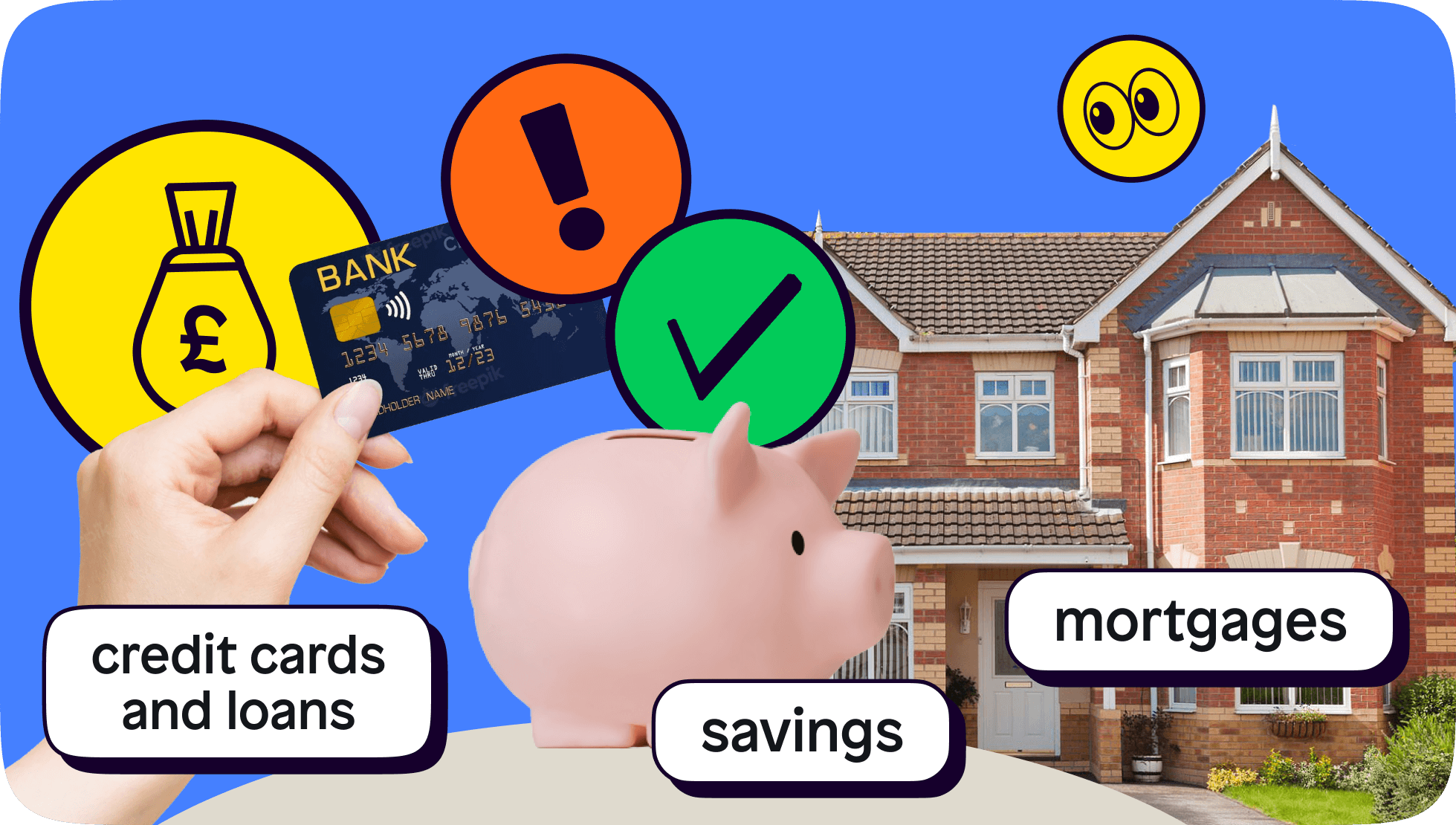

Here's some specific info on how interest rates can affect you, should you have any of the following:

🏡 Mortgages

✅ If you're on a fixed rate mortgage, your monthly payments are 'fixed' until the end of your mortgage plan, which means you won’t be hit with a larger monthly payment

❌ If you have a variable mortgage (a mortgage that changes price each month on the current interest rate), your monthly repayments are decided based on the current interest rate. When the rate rises, so will your mortgage which is a bad thing

According to the BBC, those on a tracker mortgage (a type of variable mortgage) will pay around £74 more a month, whilst those on a standard variable will experience a £46 jump, on average.

A high interest rate means obtaining a mortgage will become more expensive. Similarly, people who are on a variable mortgage will experience higher repayments.

💳 Credit cards and loans

❌ Applying the same logic, a higher interest rate means it becomes more expensive to borrow money. Taking out a loan, or repaying a variable loan will be now be more expensive

🐷 Savings

✅ Savings accounts will have favourable interest rates, which is good news if you're looking to tie up your cash in something like an ISA

Why does the Bank of England increase interest rates?

Simply put, they're trying to lower inflation. But how are the two connected?

When borrowing money becomes more expensive, fewer people do it. Makes sense, right?

Well, when all of us have less cash to spend, we save more and the economy 'slows down'. Less spending equals a cheaper economy, as businesses compete to get us to spend.

That's the bank’s hope, anyway!

And if this does happen, some groups of people will have to suffer. In this case, it'll most likely be small business owners who won’t be able to survive.

It's for this reason the Bank of England has a balancing act on their hands. Slow down the economy too much, and businesses will struggle; a lot. Don't do anything at all? Inflation would continue to rise at rapid rates and people will struggle; a lot.

Should I invest now?

There's a lot going on with the U.K's finances right now. Inflation is at a high, interest rates are at a high, and we're going through Chancellors of the Exchequer quicker than I can type this article out.

And the truth is, there are both reasons why someone might invest now, and why someone might not, depending on their perspective and situation.

The Bank of England has increased interest rates to help reduce inflation. If inflation drops, then it's likely the economy will pick up, making stock investors pretty happy in the long-term.

Unfortunately though, an increase in interest rates will make the cost of living even more expensive in the short-term which is bad for stock prices as businesses will likely suffer. Often, investors pull their money from the markets to reduce the risk of losing a large amount.

When a mass sell off like this happens, supply outweighs demand; causing prices in the market to drop which is good news for people who want to buy into the market, but bad news for people already invested in the market!

All in all, we have no idea if now is a good time to invest. No one does. What we do know is there are things you can focus on to help you make a decision. Read more on when is a good time to buy stocks to help make a well-informed and educated decision!

So, how should I invest?

The moment you've been waiting for. How’s best to invest?

Well, it all comes down to weighing up the facts, with your own perspective.

🤓 Facts:

The Bank of England's aim is to reduce consumer spending to help decrease inflation

Businesses and people will have to pay more to borrow money

Savings accounts will receive better interest rates

🧐 This could mean the following:

Stock prices will fall in the short-term due to businesses making less profit and people selling their assets to free up cash

A lot of investing is about making informed decisions based on the future state of the economy. Because of this, some stocks may perform better than others, but it’s impossible to say which.

Here are some things to keep in mind though:

Growth stocks – these require more capital to grow and their stock price is based on their future valuation, not their current valuation. Often, in times of economic difficulty, current evaluation is what maintains a stock’s price.

Value stocks – unlike growth, these have a high current valuation which can help ride the wave of a downward market

Non-cyclical stocks – typically, these tend to perform well during difficult times, as they produce essentials like food, water and clothes which people will always need.

Dividend stocks – investors may pull their money from dividends, and opt for a savings account to receive a more stable, fixed income.

Banks – banks allow people to borrow money. When this becomes more expensive, banks profit more. It may be an interesting time to see how public banking companies perform.

That's why with investing, we can apply all the theory in the world, and the result can end up being totally different. It's why your capital is always at risk.

What about cryptocurrency?

Crypto hasn't experienced a point in time when inflation and interest rates are high, so we have no historical data to support our points. We know the market has been down recently though, and with a younger demographic invested in it, it would be tough for the market to return to all-time highs.

Do any of these assets beat a savings account? That’s for you to decide.

Overall, all things connected to money often go full circle. When one person experiences a falling market, another might see it as a chance to buy the dip. Regardless of which asset you have your eye on, dollar-cost averaging offers a more steady way to invest during a very unpredictable time.

Download the Shares app and make sure to follow us on our socials 👇

As with all investing, your capital is at risk.

Shares is a trading name of Shares App Ltd. Shares App Ltd is an appointed representative of RiskSave Technologies Ltd, which is authorised and regulated by the Financial Conduct Authority.