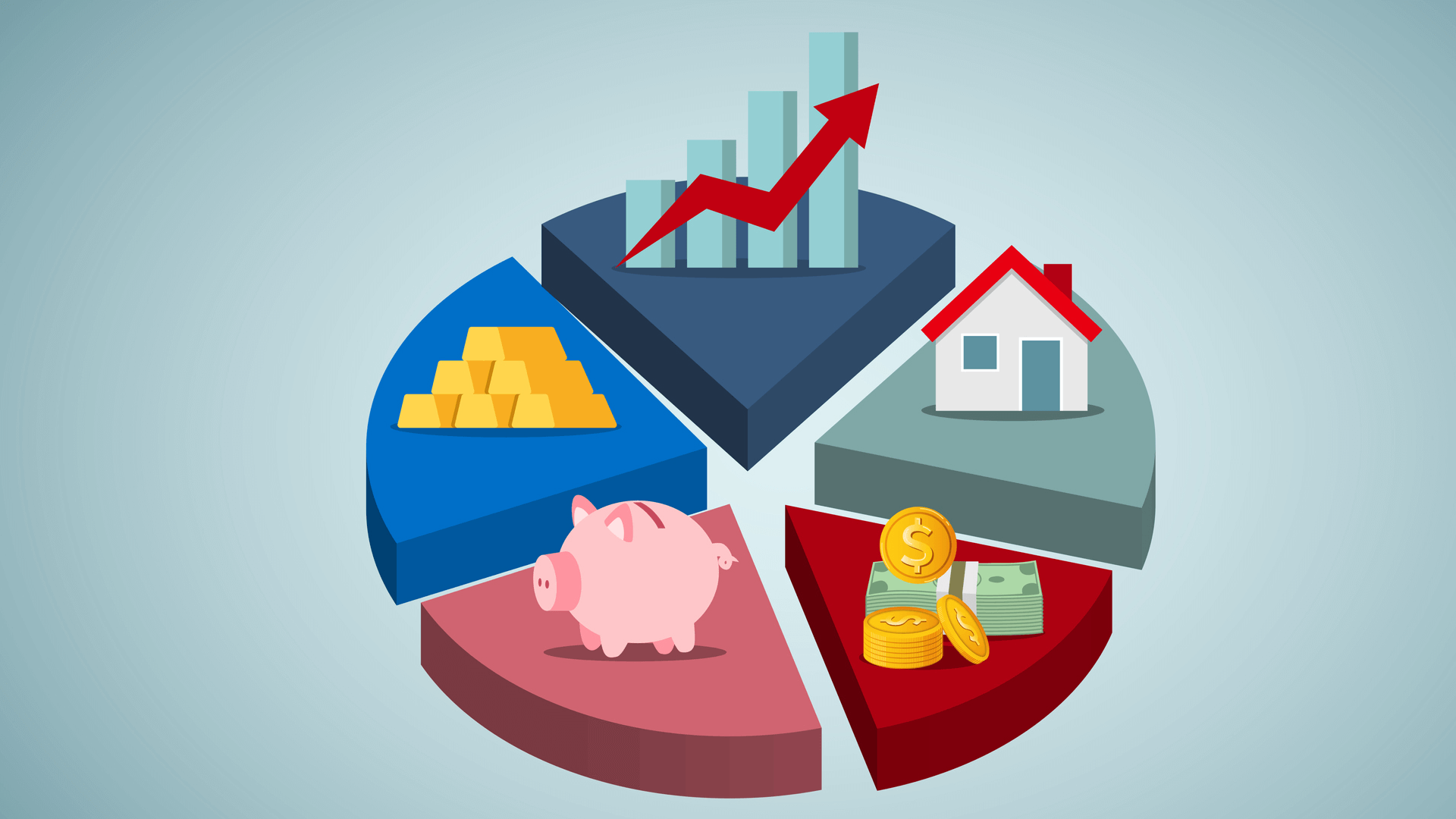

Here, we'll be guiding you through what kind of things you can invest in, otherwise known as 'investing asset classes'. I know right, who doesn't love a bit of fancy jargon.

In this article, we'll talk you through each of the follow asset classes that you can invest in.

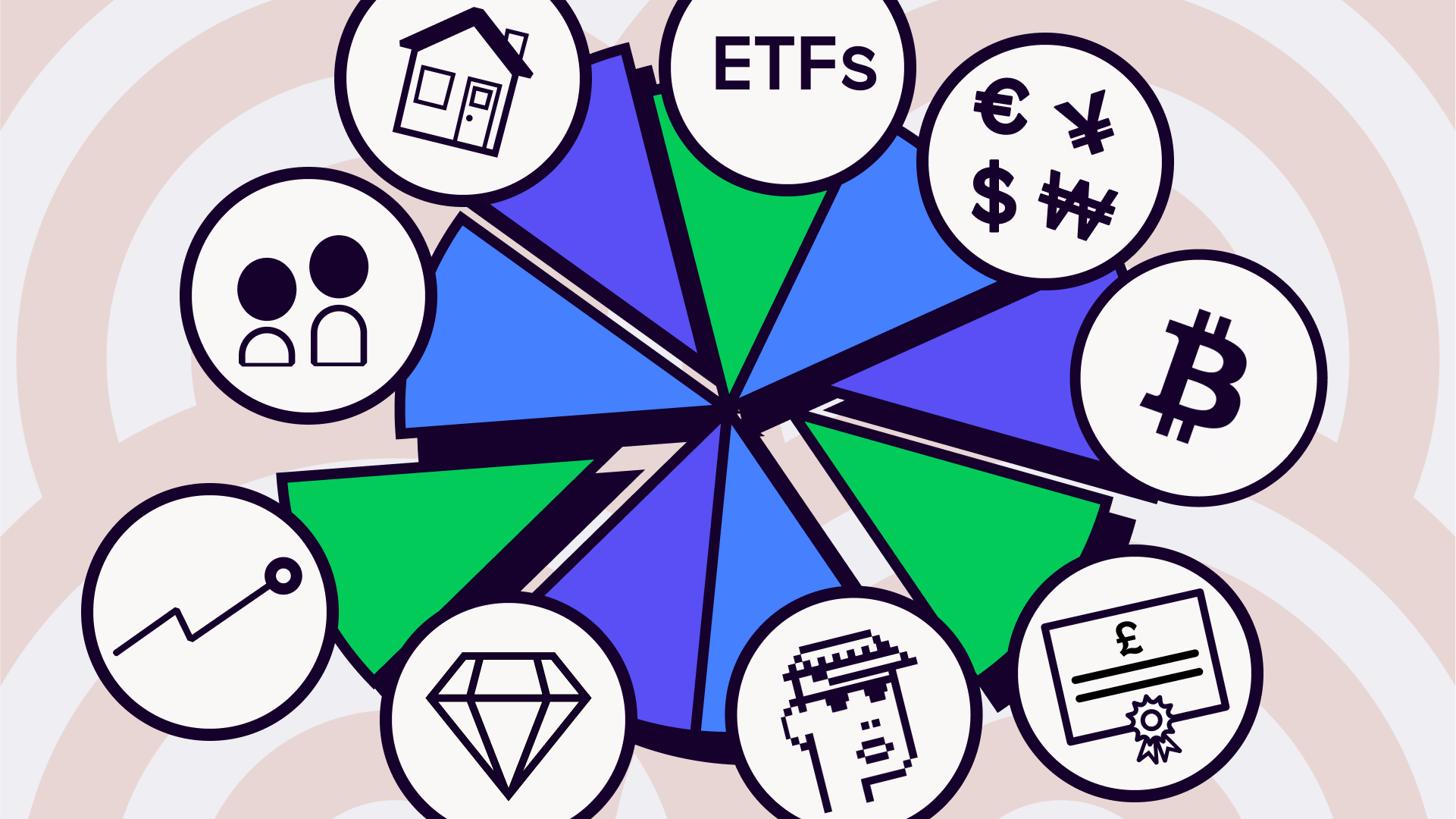

What are examples of portfolio investment entities?

Stocks and shares

ETFs

Mutual funds

Bonds

Commodities

Cryptocurrency

NFTs

Forex

Property

Stocks and shares

Stocks and shares are the most popular asset to invest in.

When you buy a share, you’re buying part ownership of the company you buy the share in. So you can own a little slice of Apple, Tesla, Lululemon - whatever you decide. It’s called having ‘equity’ in a company.

When you own a little bit of a company, you join in with its ups and downs. Apple could sell loads of iPhones, report record profits, and its share price could go up. Or, it could run into production issues, report a loss, and its share price could go down.

At its simplest, you make money from shares if you buy them at a low price and sell them at a higher price. The profit you get is called a capital gain.

There are other means of making money through stocks and shares. We talk more on this in our article about what dividend stocks are.

But before you start trying to invest in your favourite brands, know that the company has to be 'public' which means they’re listed on the stock market. If they aren't, then they're referred to as a 'private company'. Unfortunately, you can't invest in private companies.

The good news is you can check which companies are on the stock market on the Shares app.

ETFs

An ETF stands for 'exchange-traded fund'. Oh yes, more jargon to get the investing blood flowing.

ETFs can also be purchased on the stock exchange, but unlike a stock they track a wide range of assets and sectors meaning they aren't limited to one company. They can even be structured to track certain investment strategies.

Investors like to look at ETFs when they want more exposure to a sector, or even an entire asset class. For example, stocks and shares in general may have a great year in terms of return in the U.S., but it's not to say every single stock would have performed well. If someone wants to invest in the U.S.' stock market as a whole, they may look towards an ETF.

Of course, this is just one example of what an ETF could look like. Here are some other ETF examples:

A large company ETF - The SPDR S&P 500 (known as the “Spider”) is the most widely known ETF that tracks the S&P 500 Index, which is 500 of the largest companies listed on stock exchanges in the U.S.

Real estate ETF - These may hold a variety of real estate investment trust stocks

Commodity ETFs - These represent commodity markets, including gold, silver, oils and more

Mutual funds

Mutual funds also allow you to invest in a wide range of assets. But they are operated by individual professionals with fancy job titles like portfolio managers, asset managers or investment managers.

They allocate the funds with an effort to produce a return. What they invest in and how much risk they take is all outlined in something called a prospectus.

Mutual funds allow individual investors to access portfolios managed by professionals, should they not want to make investment decisions themselves. Sounds a bit risky giving someone else that amount of power of your money, right? Well, most funds are part of larger companies like Fidelity Investments and Vanguard. These accredited companies have employees who act as fund managers and are legally obliged to work in the best interest of us, the investors.

Bonds

If you have quite a low risk appetite, bonds may be an asset class to focus on.

They're a 'fixed-income instrument', meaning they act similar to an I.O.U (I owe you). They are loans made by an investor (you and me) to a borrower (typically governments and businesses). Governments often issue bonds when they need to raise capital to help build infrastructure such as roads, buildings and schools.

Investing in bonds is a bit like acting as a loan shark. Your money goes towards something somebody else needs, and they pay you back in stages. Of course, you receive interest over time to make it worth your while.

In a really simple example, let's say the government requires £12,000. I give them £12,000 and they repay me with a 2.5% interest rate of return over one year.

If they were to repay me with no interest rate, I'd receive £1,000 each month. With a 2.5% interest rate, I'd receive £1,025 a year instead, meaning I'd profit £300 by the end of the year (because 25 x 12 = 300).

Most bonds have the following outlined from the beginning:

Initial price/ face value – how much the bond costs

Coupon rate – the % of interest you receive with each repayment. In most cases, this won’t change after the bond is issued

Coupon date – which dates you're paid back on (and how often)

Yield – this is a measure of interest that takes into account the bond's fluctuating changes in value

Maturity date – the date the final repayment is made

Secondary price – the amount the bond would currently cost on the secondary market

Commodities

Commodities are natural resources that can be grown, mined or processed and are often needed when creating food, clothing or energy.

There are two main types of commodities:

Soft - these are often grown. Examples include meat, coffee, wheat and corn

Hard - these commodities are mined or extracted. Metals like gold, silver and lithium would be some examples

While it’s possible to trade in physical commodities, it’s impractical for an investor. Instead, 'futures contracts' are used. Producers and investors agree a price and set a future date when the commodity must be bought/ sold.

So, if I believe gold prices will increase, I might buy a futures contract in gold. I've locked in the price, in hope it'll be worth more by the time I have to sell it (a specified date in the future).

Commodity traders will study the markets and have the intention to buy low and sell high. Whereas long-term investing in commodities is usually done as a hedge against inflation or to diversify a portfolio.

Cryptocurrency

If your risk appetite is a little larger, then cryptocurrency may be an asset to explore.

A cryptocurrency is a digital currency, meaning it can't be physically touched like a £5 note can; it only exists through a computer network. This network isn't controlled by a 'centralised' body (such as a government or bank), rather, people collectively work together to maintain it. People doing this are known as a 'peer-to-peer' network.

There are a lot of cryptos out there, each attempting to do different things. As an investor, the key part is to look at what problem a project is trying to solve.

In the case of Bitcoin (BTC), it's the biggest cryptocurrency with a market cap of $471 billion, and aims to replace cash as we know it. Unlike cash, there are a finite amount of bitcoins (there can only ever be 21 million) which stops governments being able to print money and cause inflation.

In an ever-increasing digital world, Bitcoin has caught the attention of many investors, though it is criticised for its environmental impact upon the environment based on how much energy it consumes.

Whilst Bitcoin is crypto's poster boy, projects like Ethereum, Cardano and Solana are focused on creating blockchains to help build decentralised apps; a completely different kind of objective. Want to know more? Read our piece on what is the blockchain.

NFTs

Web 3 and the metaverse are areas that are emerging into our lives quicker than we can say Mark Zuckerberg's Horizon Worlds.

If we've learnt anything from the dot.com bubble though, it's that emerging technologies can present plenty of investment opportunities.

The latest of these in the Web 3 space are Non-fungible tokens, or NFTs for short.

If you open up 'Documents' on your Windows laptop, or 'Finder' on your Mac, you'll see a load of digital files. These might be JPEG photos from your family holiday in Portugal back in 2008, or MP4 videos of your dog. Heck, you might even have MP3 files on there if you're a music maker on SoundCloud.

These digital files that live on your computer can be 'minted' into NFTs. When an NFT is minted, it is stored onto a blockchain, which basically means you have living proof there is only one of these digital assets in existence. Sure, someone can copy and paste your photo, but the blockchain acts as your proof of ownership, much like a verification code.

As you can imagine, anything can become an NFT and we're only just getting started with their potential. The trick of the trade? Cut through the noise and find investable projects that have real utility and meaning.

Like cryptocurrency, the NFT market is volatile. Very volatile indeed.

Forex

Forex stands for 'foreign exchange', which relates to the price traditional currencies like the pound and the U.S. dollar are trading at. It is also seen as a riskier investment asset.

At its heart, forex is all about changing one currency to another. This is done for reasons like business, trading and tourism.

When trading in forex, currencies go against each other as 'exchange rate pairs'. For example, EUR/USD is a currency pair for trading the euro against the U.S. dollar.

Investors will trade forex based on what they will think will happen to a country's currency at an international level. Given it's difficult to predict what will move an international market, forex can be unpredictable which is why it has gained a risky status. Geopolitical events and to diversify portfolios are among the main reasons why people tend to invest.

In the case of the U.K, we saw Liz Truss announce her economic plans in October 2022. As these plans weren't well received, the value of the pound fell. Those who doubted her economic plans before they were unveiled may have hedged against the pound, and likely profited.

Property

If investing in property interests you, then it's worth exploring a buy-to-let investment, should you be in the position to do so.

The way it works is simple. You buy a property and rent it out.

If you've bought the property outright, then you can assume most of the rent will be landing straight into your back pocket. If you've taken out a mortgage, you will have to pay this back through a repayment mortgage or interest only mortgage.

A lot of us want to invest in property, but with house prices so high it's taking an age for many to get their first one, let alone a second as an investment. So where should you start to get a foot on the elusive property ladder?

Well, the government offers a Lifetime ISA (LISA) to help with saving for your first property.

However much you save during a year in a LISA, the government will match it by 25%. There is a maximum limit though, and that is £4,000. You can only withdraw savings from the LISA for three reasons:

It's going towards your first property purchase

You have a terminal illness

You're over the age of 60

It might not sound like a lot given how expensive properties are nowadays, but it's essentially free money if you're already saving for your first property!

For more beginner guides to do with investing, make sure to check out:

For specfic guides on asset classes, then visit our articles on:

And there you have it, nine asset classes explained! Which one is your favourite? Let us know over on the Shares app.

Make sure to follow us on our socials 👇

As with all investing, your capital is at risk.

Shares is a trading name of Shares App Ltd. Shares App Ltd is an appointed representative of RiskSave Technologies Ltd, which is authorised and regulated by the Financial Conduct Authority.